Have you ever wondered who really owns and controls global capital? You’re not alone. The world of finance is fraught with complexities and is ever evolving. Passionate about economics and the world of finance, Albina Gibadullina majored in finance during their undergraduate studies. As they progressed in their studies and began to learn of some of the socially harmful activities the financial sector perpetuates and directly benefits from, their focus shifted.

“Learning about the nature of finance raised lots of questions about what it is. I became interested in understanding how and why finance became so powerful and profitable.” Gibadullina reflects.

“Learning about the nature of finance raised lots of questions about what it is. I became interested in understanding how and why finance became so powerful and profitable.” Gibadullina reflects.

“Learning about the nature of finance raised lots of questions about what it is. I became interested in understanding how and why finance became so powerful and profitable.” Gibadullina reflects.Finding a critical space that approached the financial world from a geographical and historical perspective, Gibadullina is now a PhD candidate studying the political economy of global finance, under the supervision of Jamie Peck, Elvin Wyly, and Luke Bergmann. So what exactly does ‘finance’ encompass? Gibadullina proposes that the financial sector is composed of the financial institutions engaged in any of the three following activities: credit intermediation (lending to firms or households), market mediation (creating, participating in, and overseeing various financial markets), and rentierism (profiting from the ownership of assets). Financial intuitions involved in credit intermediation make money from the interest charged on loans. Income is generated in market mediation activities from various service fees. Rentierism is a passive activity where institutions receive income through the ownership of assets, for instance in the form of dividends, capital gains, or interest received on tradeable debt securities.

By analyzing historical financial sector data and comparing the trends between financial activities and profit margins, in a paper published during their master’s studies, Rent and financial accumulation: locating the profitability of American finance, Gibadullina made an interesting discovery. “The primary reason why the US financial sector became so profitable as a whole since the 1980s was largely because of the rise of rentier activities, rather than lending or market mediation,” states Gibadullina.

The rise of rentierism was a response to declining interest rates. In the 1980s, following a financial deregulatory wave in the US, interest rates were quite high, making lending profitable. Interest rates entered a period of decline throughout 1990s to 2010s as a result of expansionary monetary policy. And rates have remained low until very recently. During this depressed interest rate period, with lending no longer profitable, financial intuitions had to look elsewhere to maintain profits.

“Changes in interest rates can have an impact on the volume of capital flowing from the bond markets to the equity markets which contributes to asset price inflation. Changes in the aggregate value of the US stock market are largely driven by speculative financial flows,” explains Gibadullina.

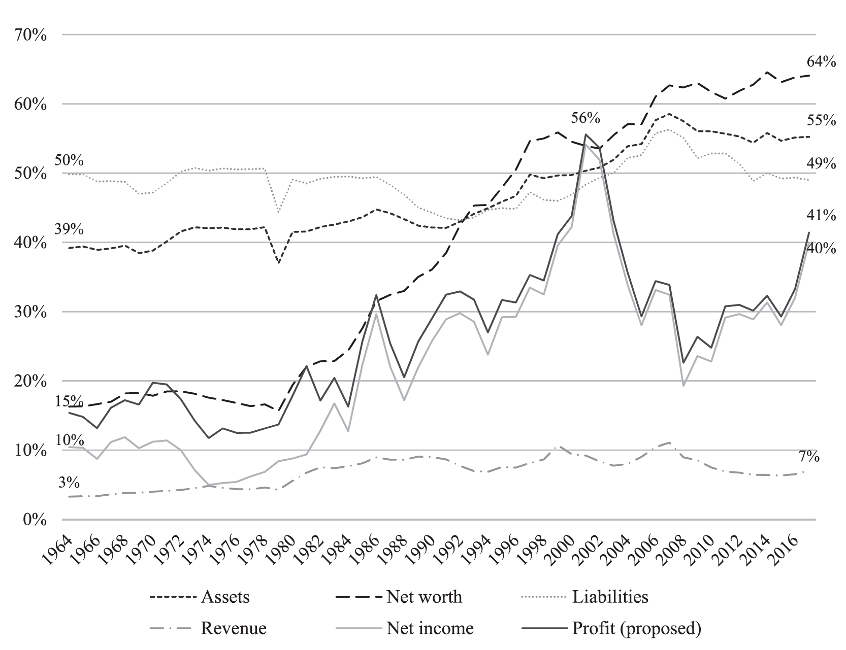

Financial institutions being owners and managers of capital is a historically unprecedented phenomenon with serious consequences. Gibadullina identified this shift in financial activities as being responsible for the skyrocketing profits in the US financial sector over the last few decades. The research shows that an estimated 64% of US corporate net worth is owned by financial institutions. This gives the financial sector unprecedented power to control the economy.

Figure 1: Finance sector share of relevant US economic aggregates.

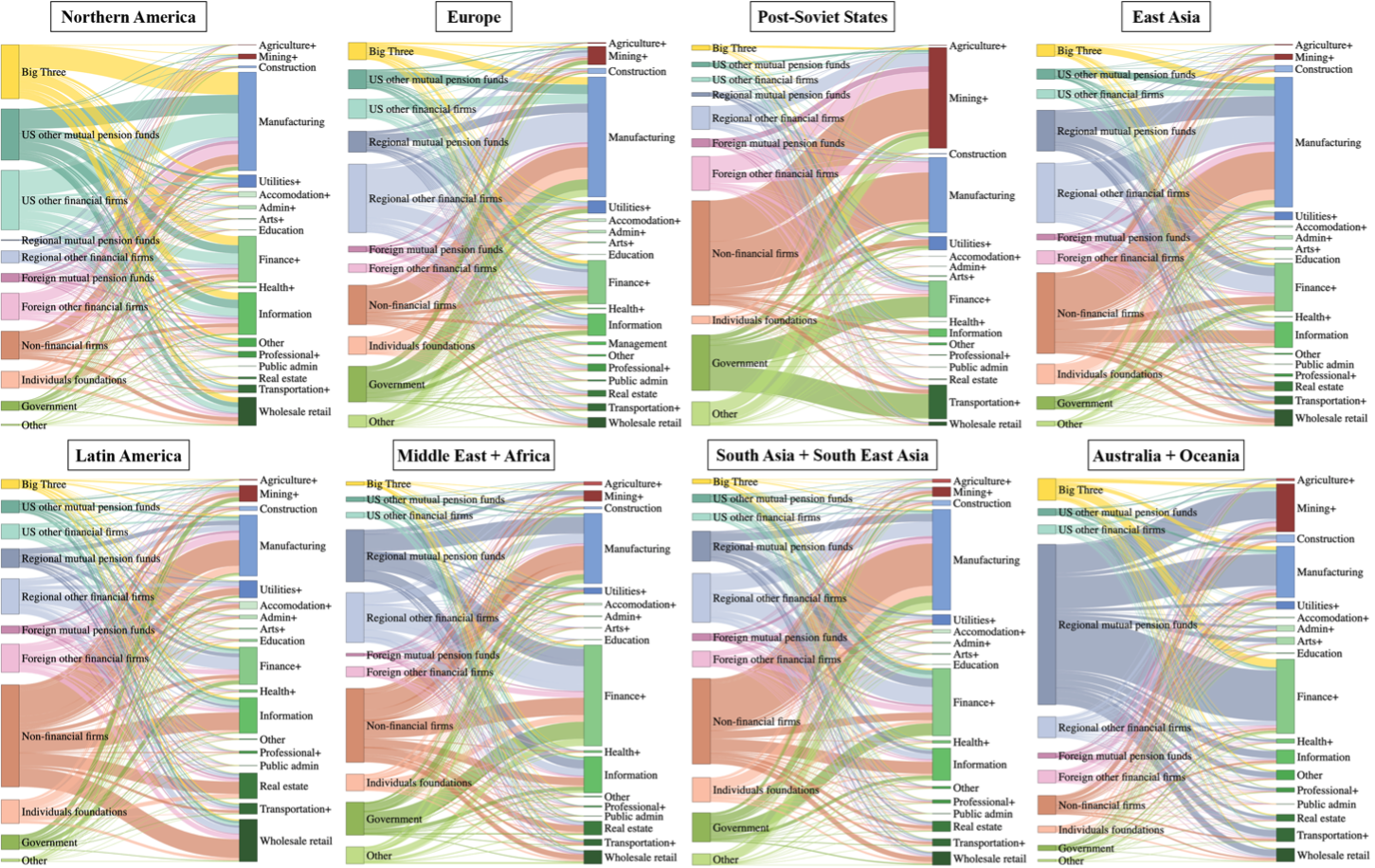

Building on these findings, Gibadullina’s recent publication, Who owns and controls global capital? Uneven geographies of asset manager capitalism, examines how much capital US funds own locally and globally. Focused on the rise of the ‘Big Three’, the three largest US asset management firms (BlackRock, Vanguard and State Street), the data reveals that the assets management industry is highly monopolized by this small group of firms specializing in passive investing. The Big Three control close to 80% of the passive investment space in the US. Technological innovations have allowed for this rise, enabling these firms to oversee savings from millions of Americans and easily invest their money without employing many people to do this work. This also allows these firms to charge lower fees, offering low-cost investment options that expand client bases and increase profits.

Altogether, the Big Three directly own 17% of the US stock market and 9% of the global stock market, with a highly geographically and sectorally uneven spread. Generally, they invest in regions that are favoured by the index providers (companies that construct investment indices) so investments end up being geographically concentrated in a few select regions.

“The research revealed that Post-Soviet states, Sub-Saharan Africa, the Middle East and South East Asia do not have a lot of investments from the Big Three. Versus Australia, Japan and the UK which account for a very large share of their investments. So, despite their passive investment approach, the Big Three are actively remaking the global geography of investments,” Gibadullina says.

Figure 2: Investments from different shareholder groups to economic sectors of a region (based on the shareholder data of globally listed companies in 2018)

The concentration of ownership of assets by a few investment firms creates a huge power imbalance. The influence these firms wield over the economy is growing and raising concerns.

“With ownership comes power. Our conceptions of traditional finance are outdated and there hasn’t been enough push to reconceptualize the new structural power of finance with this ownership lens in mind. What does it mean if two thirds of the firms in your country are owned by the same financial institutions? What kind of priorities do they bring in? Whose wellbeing do they have in mind?” asks Gibadullina.

As protected entities, with hard-to-find information about their practices that is often proprietary, and lobbyists advocating for their interests, it can be difficult for researchers like Gibadullina, let alone the general public, to dissect what is going on in the world of finance. And this is exactly what motivates Gibadullina to continue in their work.

“I’m trying to decomplexify what these companies do, understand the basis of their power and what impacts they are having on society and the economy at large,” says Gibadullina.

The research is revealing stark trends in wealth and income inequality. As the gap grows, it begs the question, is there a better way to organize our economic structures to benefit us all? The next stages of Gibadullina’s research will examine the growth drivers of the US stock market as whole, the long and short-term income and wealth distribution effects of asset manager capitalism, and if and how U.S. asset managers are governing the US economy through financial markets. Perhaps the insights gleaned from this work will help us forge a new more equitable path for our economies.